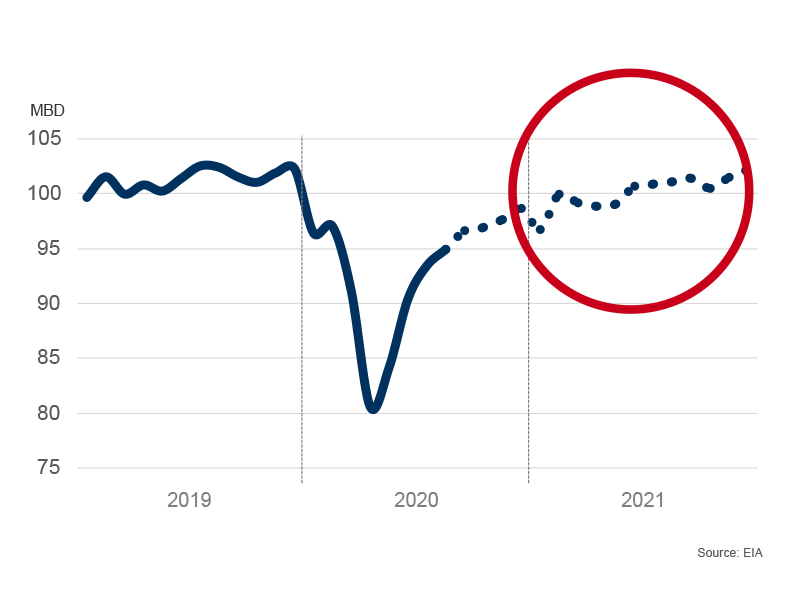

The upturn that ground to a halt... is now picking up again in 2021

As we now put summer behind us and enter autumn, we can see that tanker market development has been largely as we previously predicted – in our May market outlook and most recently in the Q2 interim report. After a particularly strong spring (driven by significant stock accumulation in response to record low oil prices), market rates fell sharply during the summer months. The sharp turnaround was attributable to reduced oil consumption (due to Covid-19), OPEC’s production cuts and stock withdrawals close to the consuming countries.

The hangover after the extensive stock accumulation between January and May is something we will have to live with for virtually the rest of the year. To summarise our view of the market for the rest of 2020, we expect the challenging market to continue during the few remaining weeks of Q3. We expect it to start improving in the latter part of Q4 – but to remain relatively mediocre overall.

If, on the other hand, we look ahead to 2021, the market looks much more exciting:

- Increased consumption of oil and falling inventories

Production and consumption of oil are obviously among the more fundamental factors behind the tanker market’s development. Since the lows in April, consumption has increased recently – steadily and relatively sharply. Statistics from the EIA indicate that consumption now stands at about 96 million barrels per day – still lower than at the turn of the year (and before the spread of Covid-19), but still significantly higher than the lows of 80/85 million barrels per day at the end of April.

According to the EIA’s forecast, oil consumption will continue to increase and at some point in spring/summer 2021 will return to pre-Covid-19 levels – i.e. about 100 million barrels per day. Obviously, this is provided no stronger “second wave” emerges, with new extensive lockdowns.

EIA: ”Back to normal oil consumption in 2021”

- The combination of increased oil consumption and continuing production cuts also means that the stocks that were built up during spring are now gradually falling. We expect them to be down to the five-year average by late 2020/early 2021. In terms of tanker market development in the longer term, this is both necessary and good.

- Strong increase in demand for tankers…

Overall, increased oil consumption and normalised stock levels create good incentives for increased demand for tanker transport. Our assessment, which is shared by many other analysts, is that we will see a sharp increase in demand of 5-10 percent in 2021, perhaps even over 10 percent initially. Whenever there are fluctuations in the tanker market, they are usually significant.

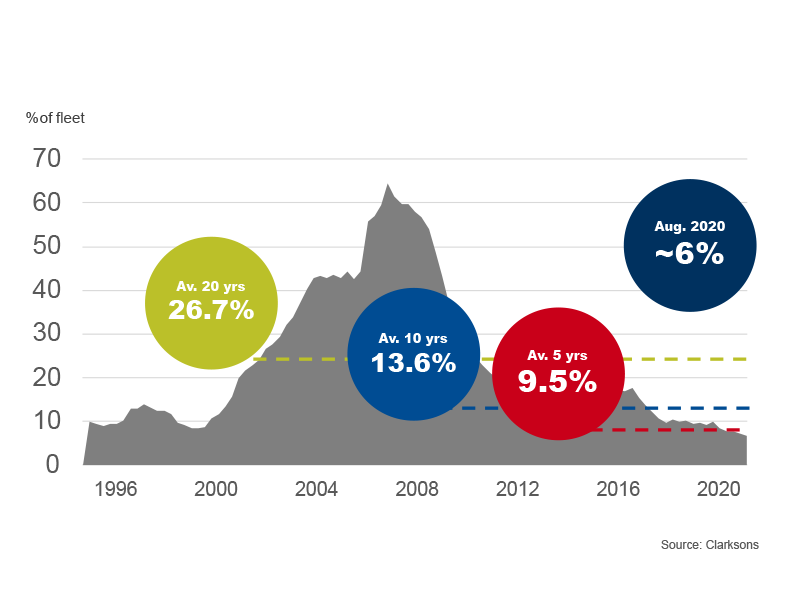

- … and record low net fleet growth

Then we have fleet development – and here the picture looks very positive. At the beginning of September 2020, the order book for the product tanker segment was at a record low 6 percent of the total tanker fleet – the lowest in over 25 years. Including the expected phasing out of tonnage, growth in 2021 is expected to be only about 2 percent. In the current situation, virtually no new orders are being placed either, which means that the low growth rate will be gradually extended. This is obviously good for the tanker market as a whole.

Record low orderbook ((Product tanker >10K)

Overall, this means that our view of 2021 is positive. Sharply rising demand for tanker transport (due to the combination of increasing oil consumption and normalised stock levels) and low net fleet growth create good conditions for a strong tanker market.

Kim Ullman,

CEO